VAT for Private Hire Drivers UK: Uber, Bolt, and Independent Operators Explained

Private hire drivers in the UK, including Uber, Bolt, and Free Now, are increasingly asked to provide their VAT registration number. Understanding whether VAT registration is necessary, which VAT schemes apply, and what expenses can be reclaimed is crucial for compliance and maximizing profits.

This guide explains VAT obligations for both Uber subcontractors and independent private hire operators, using HMRC-compliant guidance.

1. Should a Private Hire Driver Become VAT Registered?

VAT registration is mandatory if your taxable turnover exceeds £90,000 in any rolling 12-month period. Registration is optional below this threshold.

Key point: Whether VAT registration benefits you depends on whether you are the VAT supplier of the journey.

Uber/Bolt/Free Now drivers: Typically subcontractors. Uber is the VAT supplier, so registration is generally not required.

Independent operators taking direct bookings from passengers: You are the VAT supplier and may benefit from registration, especially if your business has high VATable expenses.

Benefits of VAT registration (if applicable):

Reclaim VAT on eligible business expenses.

Improve credibility with corporate clients.

Potentially reduce VAT costs on high-expense operations.

Drawbacks:

Quarterly VAT return administration.

Must charge VAT on taxable supplies if invoicing businesses.

Uber-only drivers cannot charge VAT or reclaim VAT on Uber-related expenses.

2. VAT Schemes for Private Hire Drivers

a) Standard VAT Scheme

The standard VAT scheme allows you to:

Charge VAT on taxable supplies.

Reclaim VAT on eligible business expenses.

Important: This applies only if you are the supplier of the journey.

Eligible expenses (if supplier):

Fuel

Vehicle insurance

Repairs and maintenance

Home office/phone costs

Example:

Independent operator earns £90,000/year via direct bookings.

Business expenses: £10,000 (fuel, insurance, maintenance).

VAT on earnings: £90,000 × 20% = £18,000

VAT reclaimable on expenses: £10,000 × 20% = £2,000

Net VAT due: £16,000

Uber-only drivers cannot apply Standard VAT because Uber is the supplier.

b) Flat Rate Scheme (FRS)

Designed for small businesses with turnover ≤ £150,000 (excluding VAT).

Pay a fixed percentage of turnover to HMRC instead of calculating VAT on each supply.

Flat rate for passenger transport: 10% (first-year discount: 9%).

Cannot reclaim VAT on most expenses (except capital assets over £2,000).

Important: Only usable if you are the VAT supplier. Uber-only drivers cannot use FRS.

Advantages:

Simpler VAT calculations

Predictable VAT payments

Disadvantages:

Cannot reclaim VAT on fuel, repairs, insurance

May be less beneficial than Standard VAT for high-expense businesses

Example (independent operator using FRS):

Turnover: £90,000 (including VAT)

FRS rate: 10% → VAT due: £9,000

Cannot reclaim VAT on expenses → simpler but potentially less beneficial than Standard VAT.

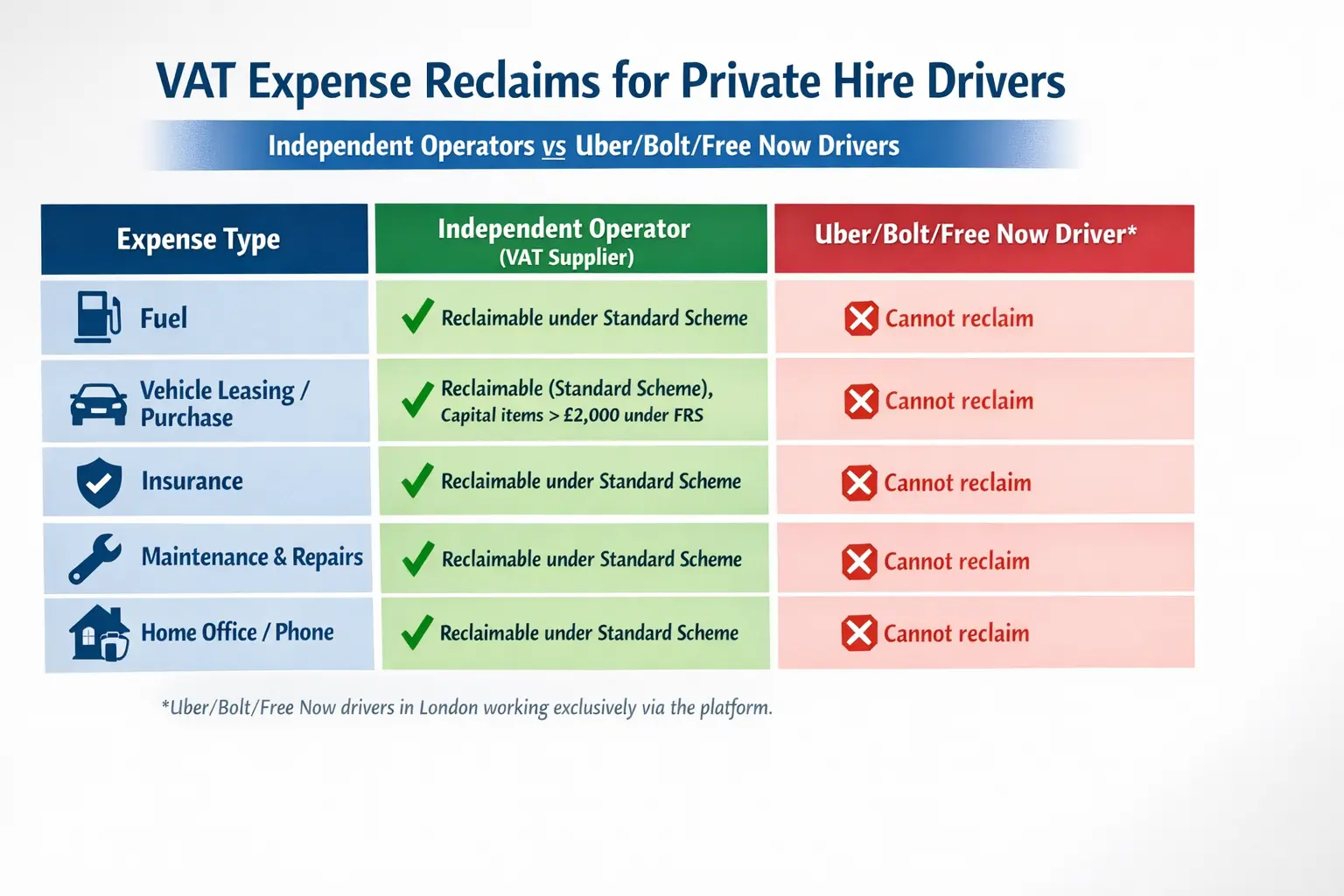

3. VAT on Private Hire Driver Expenses

Fuel:

Standard Scheme: Reclaimable if you are the VAT supplier.

Flat Rate Scheme: Only reclaimable for capital items over £2,000.

Uber-only Driver: ❌ Cannot reclaim.

Vehicle Leasing / Purchase:

Standard Scheme: Reclaimable if you are the VAT supplier.

Flat Rate Scheme: Only reclaimable for capital items over £2,000.

Uber-only Driver: ❌ Cannot reclaim.

Maintenance & Repairs:

Standard Scheme: Reclaimable if you are the VAT supplier.

Flat Rate Scheme: Not reclaimable.

Uber-only Driver: ❌ Cannot reclaim.

Home Office / Phone Costs:

Standard Scheme: Reclaimable if you are the VAT supplier.

Flat Rate Scheme: Not reclaimable.

Uber-only Driver: ❌ Cannot reclaim.

*Uber/Bolt/Free Now drivers working exclusively via the platform in London.

Tip: High-expense independent operators may benefit more from the Standard VAT Scheme than FRS. Uber-only drivers cannot reclaim VAT on platform-related expenses.

4. Key Takeaways for Private Hire Drivers

VAT registration is mandatory only if turnover > £90,000 and you are the supplier of the journey.

Most Uber drivers are subcontractors, so registration is usually unnecessary.

Standard VAT scheme allows reclaiming VAT on expenses, but only if you are the supplier.

Flat Rate Scheme is simpler but limits VAT recovery and is not usable for Uber-only drivers.

Uber may request your VAT number for self-billing, but this does not make you the VAT supplier.

Independent operators with direct bookings and high expenses may benefit from Standard VAT.

5. FAQ: VAT for Private Hire Drivers

Q1: Do I have to register for VAT as a private hire driver?

A1: Only if your taxable turnover exceeds £90,000 and you are the supplier of the journey.

Q2: Can I use the Flat Rate Scheme as an Uber driver?

A2: No. FRS is only for VAT-registered suppliers. Most Uber drivers are subcontractors and cannot use it.

Q3: Can I reclaim VAT on fuel or car maintenance?

A3: Only if you are the VAT supplier to passengers and registered. Uber-only drivers cannot reclaim VAT on platform-related expenses.

Q4: Uber offers to pay VAT on my earnings — should I register?

A4: Uber paying VAT is an accounting/self-billing mechanism. It does not change your VAT obligations. Registration is only required if the turnover threshold is met and you are the supplier.

Q5: Should I use Standard VAT or Flat Rate Scheme?

A5: Independent operators with high expenses benefit from Standard VAT. FRS is simpler but less flexible. Uber-only drivers cannot use either.

Q6: Can I register for VAT and charge VAT on Uber fares?

A6: No. Uber is the VAT supplier. Charging VAT on passenger fares would be incorrect and non-compliant.

Q7: Is VAT registration ever beneficial for Uber drivers?

A7: Only if the driver operates independently, supplies passengers directly, and has significant VATable expenses.

6. Conclusion

For most London Uber drivers, VAT registration and schemes like Standard or Flat Rate VAT do not apply, because they are subcontractors and Uber is the VAT supplier. Independent operators who take direct bookings can benefit from registration and schemes, especially if expenses are high.

Always consult a professional accountant before registering for VAT or selecting a scheme. Incorrect VAT treatment can lead to HMRC penalties and reduce net income.

Disclaimer:

The information provided in this article is for general guidance only and is based on current HMRC rules as of January 2026. It is not a substitute for professional advice. VAT treatment can vary depending on individual circumstances. S & B Accountants Ltd, its directors, and staff accept no responsibility for any loss, tax liability, or penalties incurred as a result of acting on the information provided. Drivers are strongly advised to seek advice from a qualified accountant or tax professional before registering for VAT or selecting a VAT scheme.